The international scientific and analytical, reviewed, printing and electronic journal of Paata Gugushvili Institute of Economics of Ivane Javakhishvili Tbilisi State University

Some Issues in Improving the Organization of Labor Remuneration System in the Construction Sector of Georgia

Summary

The paper deals with the opportunities of using one of the methods of strategic analysis and organization of effective remuneration system based on it to achieve financial sustainability in the construction sector of Georgia.

Keywords: CVP Analysis, marginal income, break-even point, operational leverage, margin of safety.

Introduction

At every stage of economic activity, it is important for a businessman, when formulating a business strategy, to answer questions - how much profits are produced at a certain level of sales, also, about the minimum sales volume needed to ensure profitability, stability and growth of the company.

CVP (Cost-Volume-Profit) analysis is one of the most effective methods of strategic analysis. Most auditors and experts use it to better assess the financial performance of the company and to provide well-substantiated recommendations (on organization development strategy).

One of the objectives of the CVP analysis is to determine an optimal proportion of the fixed and variable costs of the organization in such a way as to minimize business risk.

Since a significant part of the fixed and variable costs is the remuneration of labor (in various forms), the purpose of analysis is to organize a flexible system of remuneration in the company.

Discussion

The main components of CVP analysis are:

- Marginal income – measures the difference between total revenue and variable costs of sales of products (works, services) ;

- Break-even point- the level at which total costs and total revenue from sales of products (works, services) are equal (at this point, a business neither earns any profit nor suffers any loss.);

- Operational leverage - mechanism to measure the extent of the change in operating income resulting from change in sales volume of products (works, services);

- Margin of safety - Showing the deviation from break-even point of actual profit from sales of products (works, services). [1]

As already noted above, the break-even point (BEP) is determined on the basis of the sales volume and the costs incurred. It is necessary to classify costs into fixed costs and variable costs. Variable costs (raw material, piece wage, etc ) are expenses that vary in proportion to the volume of goods or services. Fixed costs (repair and maintenance costs of equipments and buildings, lease and leasing payments, utilities costs, time salary etc.) are expenses that are not dependent on the volume of production.

The break-even point is calculated by the following formula:

![]()

A low break-even point indicates the success of the company, and its increase reflects deterioration of the Company's financial situation. However, it is possible to explicitly assert that in the case where the company scale remains unchanged since the increase in sales automatically leads to increase in fixed costs. Thus, the break-even point is not an optimal indicator of the company's success. It shows what the minimum sales should be so that the company can operate without losses, but not always reflect the financial position of the company. To do this, there is another indicator, in particular margin of safety, which is calculated by the following formula:

![]()

The margin of safety indicates the amount by which a company's sales could decrease before the company will become unprofitable. The higher the percentage of this indicator, the more stable the financial situation of the company and less dependence on market fluctuations and rising costs.

On the basis of the presented formulas, it can be concluded that the break-even point will increase when the amount of variable costs increases, but the margin of safety decreases. So, the increase in variable costs of the company (the main part of which is the piece wage) leads to a deterioration in the financial stability of the company.

When the break-even point is reached, the first profit is generated, and the management of the company is interested in its growth rate. To do this, the operational leverage is used, which is expressed in percentages and calculated by the following formula:

![]()

The degree of operational leverage is determined by the costs structure (distribution of funds between variable and fixed costs). The higher the share of fixed costs in the total costs, the higher the degree of operational leverage. A company with low operational leverage has high variable costs.

It should be noted that in case of sales growth the company with a high operational leverage increases profit at a rapid pace, but when sales shrink, a high operational leverage may drag on a company’s profits. [2,3]

It is clear that in some cases the high degree of operational leverage, i.e. the high share of fixed costs in the total costs, is not suitable for the company. This means that the dominance of time wages is in some cases harmful to the company in some cases.

According to 2013 General Industry Compensation Survey of Georgia by EY Georgia, 88% of companies are using variable components together with a fixed salary. However, it should be noted that only 41% of companies have implemented the performance evaluation system that provides an objective determination of the amount of variable compensation of management. Interestingly, the ratio of variable pay to fixed payments is 12% in ordinary workers and 15% in middle and top managers. [4]

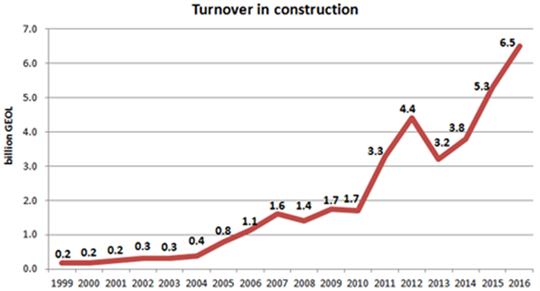

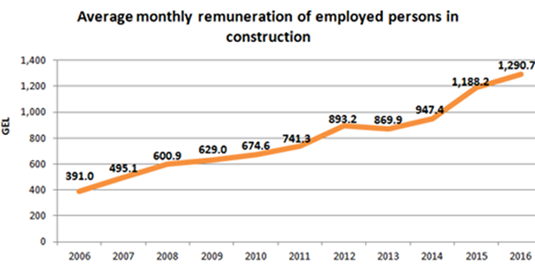

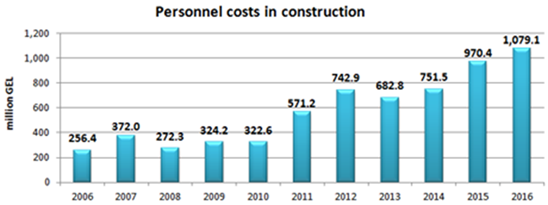

Since 2013, the stable growth in turnover and increase in labor costs is observed in the construction sector of Georgia.

According to the National Statistics Office of Georgia, the turnover in the construction sector increased from 3,2 billion GEL in 2013 to 6.5 billion GEL in 2016, or by 203%.

As for the labor costs in the field, they increased from 682.8 million GEL in 2013 to 1 079,1 million GEL in 2016, or by 158%.

The average monthly salary was 869.9 GEL in 2013 and 1290.7 GEL in 2016, which means a 148% increase. [5]

Thus, the statistics show that the growth rate of turnover in the construction sector has outpaced the growth of average monthly wages and total labor costs. That is, the time wage in the salary schedule structure prevails at the current stage.

Conclusion

In the formation of the expenditure policy in the construction sector in Georgia, it is necessary to keep proper proportion between the time and piece wages in the salary schedule, so that the company can maintain financial stability even under unstable dynamics of the sales. The best way is to use the Hay`s profile spreadsheet method (grading system) for administrative and support staff, and lump sum salary for the builders (workers, masters and others), which is the most flexible form of remuneration in terms of variable sales.

References:

- Breakeven Analysis: The Definitive Guide to Cost-Volume-Profit Analysis, Michael E. Cafferky and Jon Wentworth, Business Expert Press, 2010, pp 89-93

- Management accounting, M.K.Sanin, St.Peterburg SU ITMO, 2014, pp. 33-49

- Financial engineering, B.B. Bocharov, St.Peterburg Piter, 2004, pp. 68-74

- "Labor Market in Georgia" T. Katchakhidze, Magazine "Forbes", 2014, May

- www.geostat.com